Nobel Economist Robert Solow calculated that 80% of economic growth is the result of advances in technology. This Makes sense. Technology makes us more productive.

However, GDP measures the products, not the producers. Engineers, Scientists, and Technologists are responsible for ideation, design, and implementation of new and improved technology.

Unfortunately, Engineers, Scientists and Technologists are classified as “intangibles” Intangibles are, in turn, classified as expenses to be minimized, not investment to be maximized.

Here’s the good news… 80% of the true global economy is simply hidden from view. Trillions upon trillions of dollars are sitting on the table waiting to be measured into existence. Can you see it?

The Ingenesist Project uses game theory, blockchain, and Artificial Intelligence to convert Intangible Assets into a tangible form.

Join The Ingenesist Project

Analysis

The purpose of this video is to synthesize the simplest interpretation of value and test that against prevailing economic principals. Engineers, scientists and technologists are treated as EXPENSES, let that sink in. If they are not assets, then they are LIABILITIES… full stop. This is a clear, present and vastly consequential flaw that must be addressed by someone somewhere.

Otherwise, if there is no institution willing or able to defend this flawed economic principal, then it is super-vulnerable to disruption. We need to maximize innovation, not minimize innovation. There needs to be a wholistic and systemic approach to solving problems in the world. We must head off global systemic risks. As clever and experienced as the VC community is, they cannot be expected to pick and choose winners and losers in the next economic paradigm.

There is far more ‘money to be made’ by shifting engineers, scientists, and technologists to the ASSET column of the global balance sheet.

A firefighter is worth millions of dollars per hour preserving lives and property… but only when there is a fire. A Fire Protection Engineer can design thousands of buildings that will never burn.

In the absence of a fire, the true value of the Scientists, Engineers, and Technologists is invisible. But the value of their economic contribution continues to persist.

What if we could measure the true value of intangible assets into present value existence. A massive new asset class would be unlocked.

The Ingenesist Project uses Game Theory, Blockchain, and Artificial Intelligence to convert intangible assets into tangible form, at scale. There is no shortage of money, only a shortage of imagination.

Join The Ingenesist Project

Analysis

The purpose of this video is to demonstrate how engineers, scientists, and technologists remove RISK from complex systems. Risk is directly correlated to “return” and, therefore, profits.

So what happens to all of that value that a single diligent engineer creates when they remove all of the risk? Is it paid to the engineer? no. Is it returned to the non-victims of the calamity averted? no. Is captured by the the banking system as some form of arbitrage? Yes, absolutely, yes.

This is the deep dark secrets of finance. Don’t let the engineers, scientists, and technologists know that they are paid 2-20% of what they are worth. They may want free stuff like healthcare, job security, or royalties, or else they’ll go build something else that pays better social dividends. Can’t have that.

Obviously the question becomes, what happens when there are no more engineers to eliminate risk? There is a tipping point and we are dangerously close to approaching it. These things are easy to measure, assess, and resolve but there needs to be an institution able to secure material facts and assert the economics of those facts.

What if there was a tiny and nearly imperceptible flaw in Market Capitalism that could be easily corrected? To do so would solve many of society’s most pressing needs without disrupting the institutions upon which we depend.

Technological change must always precede economic growth. We are going about the business of civilization as if economic growth must always precede technological change. It’s like driving a car while looking through a mirror. In other words, money is not the cause of innovation. Money is the result of innovation. The implications of this tiny flaw impacts everything from Climate Change and Social Equity to Venture Capital and Global Debt.

It started with classical economic theory. In the 1700’s economic inputs such as Land, Labor, and Capital were easy to measure. The products that resulted from these inputs were also easy to measure. However, in the 1700’s; social, creative, and intellectual inputs by humans were not so easy to measure. Accountants call them intangibles, but they are simply “invisibles”.

Today, this is an easier problem to solve. Ironically, technological Change has brought us new ways to measure intangible assets. All we need to do is convert them to a tangible form. The resulting economic growth will far exceed global debt because there is no such thing as “not enough money to innovate”. Together we can correct A Tiny Flaw

Join the Ingenesist Project.

Analysis

This is largely the initial video in the series and the first that we published. Attention should be drawn to the idea that maybe there is a tiny flaw that can be easily corrected. Instead of trying to solve every single problem that is strangling civilization as we know it, we could solve one single problem and the other problems will solve themselves.

The question becomes: are we too vested in our misery to even consider such a possibility? Are we so narcissistic to believe that our particular problem is the one that must be solved even if it worsens someone else’s problem? Are we all expecting the “other guy” to change and that will make your world work? Good luck with that.

The flaw is no tiny, so hidden, yet so obvious that it defies the imagination. All we need to do is measure ourselves differently. Who is stopping us from doing this? nobody. What law says we can’t do this? There is none. And if we do correct the flaw, who suffers? No one.

A Knowledge Inventory System; The Ingenesist Project

Have you ever wondered why the credits at the end of a movie are printed so small and scroll by so fast? The credits are not there for your benefit. The credits exist for the benefit of the movie industry.

Film production is a highly intellectual, creative, and social enterprise. In other words, Hollywood is denominated by knowledge assets. The rolling credits serve as a knowledge asset inventory system for all things needed to make the next movie.

Everything revolves around being on the credits or being known by people on the credits. This is how people find each other. The rolling credits make this possible. Not unlike a blockchain, in order to cheat the system, one must alter every instance of the celluloid reel or digital file.

Engineering, science and technology are also social, creative, and intellectual industries fueled by knowledge assets. Not unlike a blockchain, engineering processes are irreversible and immutable.

When we look at a sturdy bridge, or magnificent structure, or a brilliant piece of software, there is no easy way to find the people who are responsible for a specific element of that work. The Ingenesist Project uses game theory, blockchain, and Artificial Intelligence to create a knowledge asset inventory so that Engineers, Scientists, and Technologists can find each other.

Join The Ingenesist Project

Analysis

Engineering and science have long been compared to the Arts as a creative profession. The point of this video is to demonstrate how other creative professions deal with the intangibles gap. While the Hollywood system has its own set of pros and cons, the comparison is worthwhile. Notably, the arts often compensate creators with “royalties” while engineering, science, and technology most often pay hourly wages.

In addition, there are comparably fewer barriers, silos, or human resource management hurdles to navigate for artists. They don’t attempt to reduce a 4-dimensional performance down to a 2-dimensional CV/resumé. Instead, they can submit the 4D performance as their resumé. A great deal of efficiency is retained.

An Algorithm For Innovation; The Ingenesist Project

A useful definition allows people to identify, replicate, or measure the subject being defined. Yet the best definition we have for Innovation is basically, “You know it when you see it”.

How can we sustain our world if we cannot even define the sole instrument of change?

Have you ever had an epiphany? That ah-ha moment that comes from deep within… …when suddenly your knowledge about something grows exponentially within a very short period of time? Let’s call that “innovation”, where one large innovation is comprised of many smaller innovations.

In order to measure innovation, all you need to do is measure the rate of change of knowledge with respect to time. You don’t need Calculus to recognize this as an algorithm for innovation … but it helps.

If that idea doesn’t change the world, nothing will.

Join The Ingenesist Project

Analysis

Innovation is a great mystery that does not need to be. Everyone innovates – it is necessary for survival. Yet the magic and mystique of the innovator is a cultural phenomenon that forms the foundation of tech social status. Innovation is denominated in money – if you are not flush with cash, then you are not an innovator. Only VC can be innovators due to their ability to navigate financial markets. It almost seems that the more difficult it is to identify something, greater scarcity can be assigned to it. With greater scarcity come greater value. Again, when we become vested in our own misery, progress grinds to a halt.

This is all quite counter productive.

The problems of the future will require innovation, creation, new ideas, and vast execution at an astonishing scale. In order to achieve true economic sustainability, we need to a metric to denominate true value, not propped up scarcity value.

It is relatively easy to create and measure where high rates of change are occurring in a community or society. It is then relatively easy to observe what innovations take place as a result. This isn’t exactly a unicorn farm, but you probably can’t have a unicorn without these conditions in the first place. It is then only a matter of memorializing these conditions in a tangible form.

Innovation is not linear Modern civilization did not begin 10,000 years ago with 250 Trillion dollars sitting in a box somewhere in the desert.

Money was measured into existence as a function of the things that scientists, engineers, and technologists built. Innovations such as the wheel, wedge, and lever came long before the invention of International Trade Agreements Innovations in machinery, transportation and energy enabled advances in sanitation, healthcare, and computers

Yet, the wheel, wedge, and lever are more important and more widely applied than ever. Wouldn’t it make more sense if we developed a monetary system backed by the dividends of innovation rather than the gravity of debt?

The Ingenesist Project uses game theory, blockchain, and artificial intelligence to measure the true economic contribution of engineers, scientists, and technologists.

The Ingenesist Project Uses Game Theory, Blockchain, and Artificial Intelligence to convert intangible assets to a more tangible form.

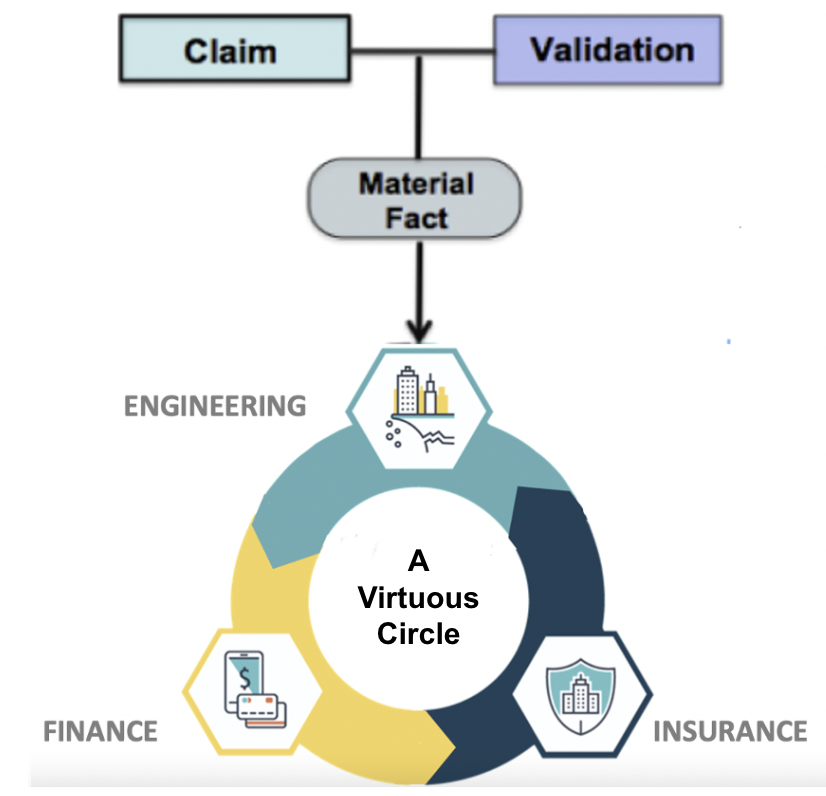

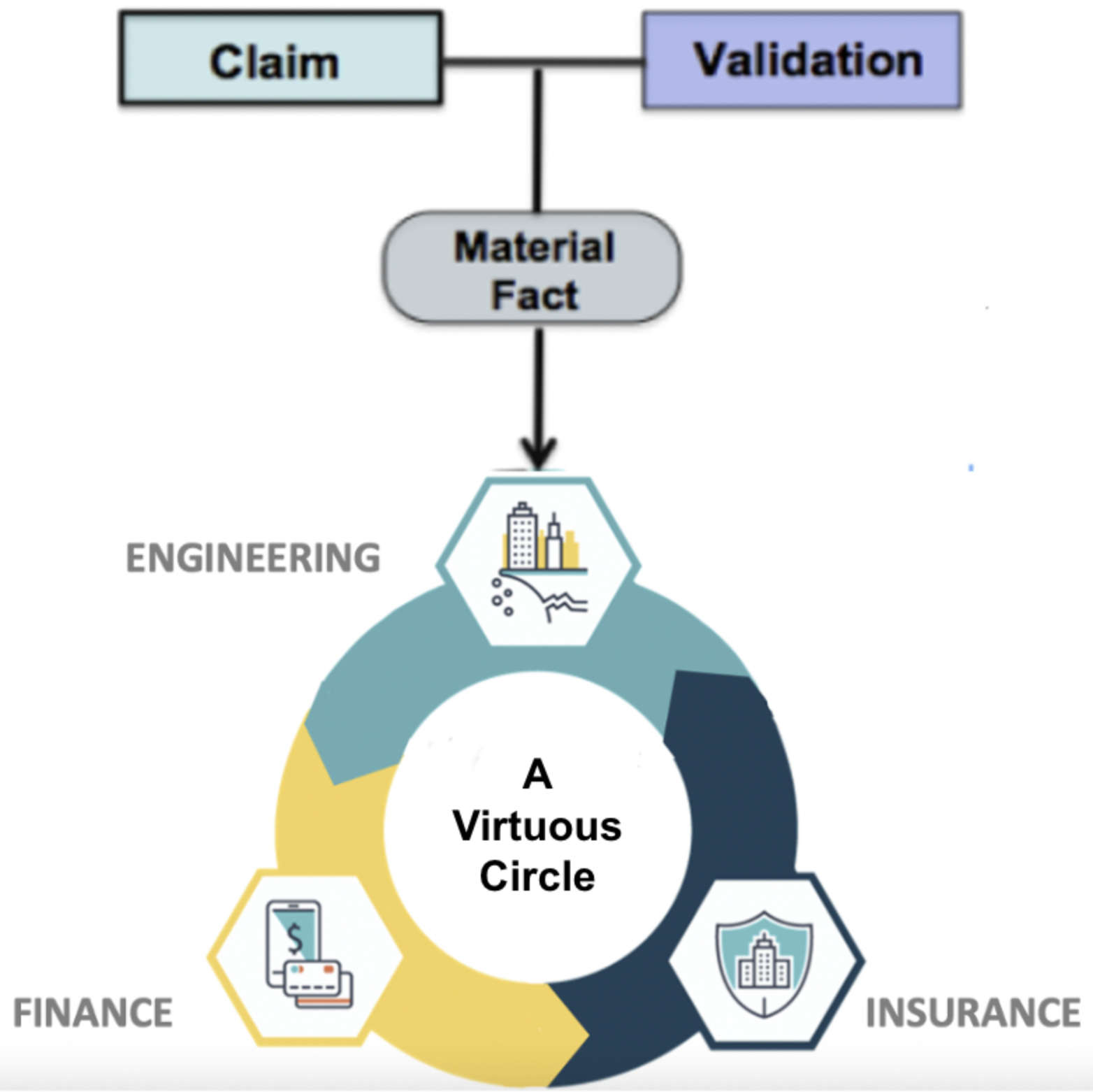

Part One: Observe The game is based on a system of claims and validations among a population of players.

Part Two: Measure Blockchain acts like a giant datalogger that captures time-value data of game transactions.

Part 3: Predict The Percentile Search Engine predicts the likelihood various combinations of players would produce novel outcomes.

These three applications acting together create a virtuous circle that converts intangible assets into a more tangible form. Join The Ingenesist Project

Analysis

In almost every video, we make the statement that The Ingenesist Project uses game theory, blockchain, and AI to make intangible assets more tangible. This sounds pretty complicated, so how do you explain it in under a minute? The audience deserves to know how we intend to deliver on the promises that we are making.

The answer to this, and almost every engineering or scientific problem, boils down to making observations, measuring outcomes, and predicting future results. The same should be true here.

We’ve also stated that engineers remove risk from complex systems. Risk assessment follows a similar sequence; first you need to identify the risk exposure, then you need predict the likelihood it will manifest, then you need to measure the consequences of the event.

The game sets things into motion, the blockchain records the motion, and the AI reads the recorded motion and predicts the next point on the curve.

So what may seem like a very complicated and jargon laden geek storm is actually an extremely simply set of tasks that almost everyone already practices in the professional lives. Why reinvent the wheel?

To borrow from a famous quote: “Uber, owns no vehicles… Google and Facebook create no content… Alibaba holds no inventory… Airbnb owns no real estate….” But they have a combined value of almost 3 Trillion dollars. This is very interesting.

Whereas most companies are priced according to strict financial performance, Network platforms provide a virtual bridge that connects people to each other. They are priced proportional to the square of the number of human connections they serve.

This is known as Metcalfe’s Law of Network Value. If network platforms create a virtual bridge connecting people, why can’t we value real bridges using Metcalfe’s law? Why can’t we value roads, airports, buildings and all manner of engineering, scientific, and technological infrastructure as proportional to the connections they serve?

The Ingenesist project uses game theory, blockchain, and artificial Intelligence to convert intangible assets into a more tangible form. Join The Ingenesist Project

Analysis

We often say that Engineers, Scientists, and technologists need only to measure themselves differently in order to become “more tangible”. Most people’s eyes glaze over as if we’re living in some fantasy world. This video demonstrates that principal exactly as it happens with network platforms that are popping up everywhere around us. Really, we’re not making this up.

Metcalfe’s law arose from the telecommunications industry to measure the utility of telephone connections. The value of the network grows exponentially with the number of points in contact. Let’s start by saying that telephone networks themselves are a creation of engineering and scientific professions.

The engineering value of a bridge is equal to it’s replacement cost – so that’s what they pay engineers to create one. However, the economic value of the bridge includes every transaction, truck delivery, soccer game, doctor appointment, and math class that resulted from the ability for 10,000 people per day to cross the river.

Facebook, Google, Alibaba, AirBnB, et al, could not exist if they were valued according to their replacement cost. Imagine what amazing works of engineering, science, and innovation are non-existant today only because it is valued incorrectly.

As the saying goes, money makes the World go around. This may not be entirely true.

Where risk is high, the cost of money is high. Where risk is low, the cost of money is low. Engineers, scientists, and technologists specialize in removing risk from complex systems. So, why is there never enough money to mitigate the world’s most pressing risks?

Fortunately, all we need to do is reorganize engineers, scientists, and technologists and the money will surely follow

The Ingenesist Project uses game theory, blockchain technology, and Artificial Intelligence to reorganize the engineering and scientific professions.

This video poses a legitimate question. If there is money to be made by mitigating risk, why are Engineers, Scientists, and technologists classified as expenses (liabilities), and not assets on global balance sheets?

It’s amazing how vested we are in this staggering little flaw in market Capitalism.

Solving the problems of the future will require humans to innovate at an astonishing rate… … far greater than anything our existing economic system can support. In order to achieve this, there must be a fundamental shift in how knowledge assets are measured, curated, and exchanged.

Today, a traditional bank distributes money backed by your promise of FUTURE productivity. Innovation is also a promise backed by FUTURE productivity. Two currencies backed by the same underlying asset are readily convertible.

In the future, an Innovation Bank, would issue currency backed directly by the true value of innovation. All we need to do is measure ourselves differently.

The Ingenesist Project uses game theory, blockchain, and Artificial Intelligence to convert intangible assets into a more tangible form.

Join The Ingenesist Project

Analysis

The Innovation Standard is a reference to the Gold Standard or the Debt Standard, or the Oil Standard, etc. Whatever the standard, it needs to represent human productivity or else nobody would work in exchange for it (think about that for a sec).

The problems that face the world are global and they are systemic. That means that free markets technically don’t exist and the next thing that needs to be produced is the thing that society needs. Sure everyone wants a new Lambo, but it’s not very useful if the roads are too rough to drive it. Sure.Bitcoin is awesome but it’s contingent on a reliable energy grid. Sure, I love AI and much as the next geek but who’s going to read my content if they lack education to act on it?

Money as we know it just does not move fast enough. It does not represent the true productivity of Moms and Dads, soccer coaches, engineers, Scientists, teachers, and event organizers. Money needs to be produced as thenet sum of productive human behaviors. People know what problem needs to be solved next and if you give them the tools to fix things, they will.

Competition is one way of arriving at the optimal solution to a problem. Some call it the “Law of Nature”, survival of the fittest – where the final score can only be One to Zero. Unfortunately, in order to feed the winner, we must cultivate suitable losers. Evolution is slow and inefficient as a business optimization tool.

The laws of Nature provide infinitely more examples of collaboration than competition. Even if one player does not win today, their capacity to innovate remains to continuously improve the game for everyone later … if we let them.

The Ingenesist Project uses game theory, blockchain, and artificial intelligence to convert intangible assets into a more tangible form. Join The Ingenesist Project

Analysis:

This video acknowledges the value of competition as a solution optimization tool. So competition is not being called into question. However, a different problem involves preserving the knowledge, innovation, and wisdom that was created in the act of competition so that they can be developed in future or tangential problem solving environments.

Economics is the science of incentives which invariably invokes the discipline of game theory. we do have complete control over how a game is played, how players are preserved (or destroyed) and how equity is distributed. As such, we have complete control over the sustainability of the game which is ultimately in the best interest of everyone.

The conclusion is that a game which maximizes the health and welfare of the players ultimately maximizes the value of the game.

A bank won’t lend money to a project that is not insured. An insurance company will not underwrite a project that is not properly engineered. Engineering projects need to be financed to cover the cost of design and construction.

This is the Virtuous Circle of economic development. If any part of this cycle is broken, incomplete or corrupted, economic development fails.

Financial institutions simply issue paper receipts called “Money” to represent the actual things that engineers, scientists, and technologists create.

Money is, in fact, the intangible asset and engineering is the tangible asset! We’ve gotten it backwards.

When a virtuous circle reverses itself, it becomes a vicious circle. This is where we are today Fortunately, this is an easier problem to solve. The Ingenesist Project uses Game Theory, Blockchain, and Artificial Intelligence to reverse this vicious circle.

The purpose of this video is to introduce the big picture of how the Innovation Bank will integrate with existing financial networks to make the production cycle more efficient and more responsive to systemic risk.

The point of this video is to isolate the idea that our global economy is an interrelated system with 3 critical components that must be integrated and operating at peak efficiency in order for the economy to serve global citizens equitably.

The challenges of the future will require humans to innovate at an astonishing rate – far more rapidly than our current financial system can support. There is no way that Venture Capital – our current “best bet” – can respond to the speed, breadth, and depth of technological change.

The problem ahead is systemic risk. It is not possible for a collection of competing VC to pick the winners and the losers of the next economic paradigm. Unintentionally, the the VC system may cause more damage than good.

This idea is useful for when we introduce the game, blockchain, and AI components – the blockchain serves as a check valve that allows the virtuous circle to spin in only one direction. The game mechanics provide the energy to keep the virtuous circle spinning in the right direction, Augmented Intelligence will help identify what components of the system are operating optimally so that innovation can be applied correctly.

Decentralization is the rallying cry of the Blockchain Movement.

Few people realize that the Science, Engineering, and Technology professions are already decentralized. Unlike Banking and Finance, there are no all-powerful incumbents that must be vanquished. And the laws of Nature already apply to everyone.

Instead, Scientists, Engineers, and Technologists are contained by innumerable silos that have little to do with the Natural Laws We are segregated by jurisdiction, academia, ontology, corporations, politics, Trade Groups, Societies, international borders, and much more.

We represent 5% of the workforce but are responsible for 80% of economic growth. But collectively, we are weak, disorganized and powerless to prioritize the needs of our World. The only thing standing in our way, is ourselves. This is a much different problem than decentralization.

The Ingenesist Project uses Game Theory, Blockchain and Artificial Intelligence to remove the silos that divide us.

Analysis:

The single point of this video was to introduce the distinction that a centralized institution and a collection of compartmentalized institutions may have similar characteristics to the participants, but are not the same thing. The former is far more difficult to disrupt while the latter is entirely vulnerable to disruption. This represents a huge opportunity for those who can see the distinction.

This idea plays a central role in the execution of The Innovation Bank. Where many see a stone wall of resistance to change, there may actually exists a paper veneer.

Have you ever wondered why a soccer goal has a net? The purpose of the net is to provide a visual contrast so that 50,000 observers can immediately reach a consensus that something very important has happened.

After that, a digital token is awarded to the team that scored a goal. The digital token also secures valuable business intelligence like game strategy, player stats, league standings, revenue, and everything else.

However, the consensus is by far the most important part. With the consensus, a player can make a lot of money. Without the consensus, they are invisible. With the consensus, the community can invest in a new stadium. Without the consensus, we can only play at the school yard. With the consensus, the economy flourishes. Without the consensus, it fails.

Lots of crypto projects have these same pieces. But mostly, they are mixed up. The Ingenesist Project uses Game Theory, Blockchain, and Artificial Intelligence to secure community consensus.

Nobel Laureate Dr. Robert Solow calculated that 80% of economic growth can be attributed to technological change. This is the domain of engineers, scientists, and technologists. Accordingly, knowledge assets and their derivatives are not actually “intangible” but rather, they are simply invisible and unable to be measured directly. Like the proverbial “tip of the iceberg” the visible part of the economy is supported by the invisible assets below the surface.

True to form, emerging technology now offers us the ability to quantify this vast reservoir of value. We now have the opportunity to unlock an economy many times larger than the one we currently grapple with – the one in which there is “never enough money” to care for our planet and meet the needs of our civilization.

The Innovation Bank:

The Innovation Bank utilizes game mechanics, blockchain technology, and Artificial Intelligence to measure the natural interactions of engineers, scientists, and technologists within a simulation representing this hidden economy. Novel Financial Instruments may then represent this new value.

What is an Ingenesist?

A “Capitalist” is a person who uses money to invest in trade and industry for profit. An “Ingenesist” is a person who uses ingenuity to invest in trade and industry for profit. Both operate in tandem to arrive at optimal solutions to market requirements.

Join Us:

The Ingenesist Project comprises the collective vision, intellect, and creativity of more than 250 engineers, scientists, and technologists who have collaborated across various industries over the past 30 years as a non-profit research and governance organization.

Classical economics is built upon a scarcity model of supply and demand of physical assets. In the trade of knowledge assets, the transfer of knowledge to one party does not require the cessation of knowledge by the other. As a result, it is estimated that 80% of a modern economy is intangible simply because it is not measured in accordance with generally accepted accounting practices. New methods in Blockchain and AI allow us to measure new value assets into tangible existence. This article proposes an accounting system for the next economic paradigm.

When Bears and Bulls Collide

In conventional accounting practices, a positive entry in the asset column of a balance sheet must correspond to a negative entry in the debit column. However, Knowledge Assets (K-Assets), function differently. The transfer of K-Assets does not require deducting the asset from the previous owner. Consequently, K-Assets are abundant and necessitate a different form of accounting to correctly attribute the contributions of STEM practitioners on a balance sheet.

A Brave New GAAP:

The Innovation Bank by The Ingenesist Project, provides the substrate for the production of K-Assets. This process is similar to how financial institutions facilitate the production of Capital Assets (C-Assets), but with distinct differences. Furthermore, the successful accounting system would facilitates the equitable exchange between of K-Assets and C Assets. The goal is to establish parity between these previously separate asset classes based on an universal risk-adjusted basis, rather than a scarce profit-adjusted basis.

Revolutionizing Technology Transfer

The Innovation Bank revolutionizes technology transfer by focusing on knowledge assets in their natural state – the mind of the practitioners – rather than a physical objects like machines, buildings, or processes that they may create. Although the end result is identical, this approach proves far more efficient.

In the Innovation Bank, the K-Asset, is created when one practitioner makes a claim and another practitioner validates it on a decentralized database. As a reward, they each receive cryptographic tokens that can later be used to access system metadata or traded on an open exchange for business intelligence. This dynamic “nano-credentialization” in aggregate, forms a means to measure economic potential.

A simple game with extraordinary implications.

The system operates autonomously, providing practitioners with incentives to generate new K-Assets. The rate at which they gain access to other practitioners depends on the quality and quantity of their own K-Asset production. Practitioners are driven to maximize token rewards and accumulate a personal transaction record consisting of successful claims and validations. Access to the database opens up more opportunities for them to generate further claims and validations, creating a positive cycle of growth.

Digital Career Path

Individual transaction records essentially serve as a digital public key, representing a practitioner’s résumé, CV, or portfolio. The owner maintains full control over this record. To ensure integrity, the same game mechanics that populate the Innovation Bank discourage trivial, false, inaccurate, and malicious transactions. The ledger is immutable, auditable, and incorruptible, providing a robust system that prevents such fraudulent or malicious behavior.

The Economy of the Future

In this brave new world of accounting, where knowledge assets are valued on their intrinsic merit rather than their scarcity, the Innovation Bank represents a significant step forward. By embracing this new accounting paradigm, we can unlock the full potential of human knowledge, foster innovation, and create a more inclusive and sustainable economy for the future. Imagine the world that humanity can build for itself if the other 80% of economic growth could be measured into tangible existence.

The world is facing increasingly systemic challenges that pose significant threats to the global economy. The risk of a catastrophic event in one part of the world triggering widespread instability or collapse is now more imminent than ever. This isn’t merely a political issue; it’s an engineering challenge with the potential for a straightforward solution.

Insurance plays a vital role in ensuring the smooth operation of the global economy by providing a steady financial backbone for its builders, innovators, and participants. However, insurance can only function effectively when we have a clear understanding of known risks, their probabilities, and the consequences of potential losses. This underscores the critical importance of curating accurate and validated information about the physical state of the world.

The Domain of Engineering

Engineers, fundamentally, are professionals dedicated to reducing risk in complex systems. Interestingly, their analytical methods bear a striking resemblance to those employed by actuaries in the insurance industry. This highlights that the task of mitigating global systemic risk hinges on harnessing the expertise and observations of global engineers, scientists, and technologists.

The Age of Disinformation

In the information age, the business model predominantly revolves around collecting, manipulating, and leveraging information. Sadly, there are limited incentives to curate and verify accurate information. It’s worth noting that the absence of information can be as detrimental as false information, and both are considerably cheaper than producing and validating factual information. This is where the financial system faces significant challenges.

Converting Intangible Assets into Tangible Assets

One of the most pressing issues facing society today is the misallocation and confinement of engineers and scientists within various silos, such as academic institutions, political boundaries, corporate structures, arcane ontologies, and other factors unrelated to the natural laws equally affecting us all. Their knowledge is often categorized as “intangible assets,” not because it lacks substance, but because it’s challenging to quantify. Imagine if there were a quick and straightforward method to measure these intangible assets, transforming them into “tangible” assets, thereby creating a new asset class significantly more valuable than traditional assets.

A Straightforward Solution

The Ingenesist Project, a nonprofit professional network, is developing a platform designed to measure intangible assets and render them more tangible. Through the utilization of game theory, blockchain technology, and artificial intelligence, credible individuals make claims about the physical state of the world, which are then validated by other participants on the professional network. This dynamic process creates a validated and easily measurable large language graph, from which valuable AI business intelligence can be derived. Participants receive electronic tokens for contributing to this immutable native blockchain. The global insurance and finance industry can access this powerful network graph by purchasing tokens on a third-party clearinghouse from those seeking to sell them, with token value determined by market supply and demand.

Vast Consequences

By introducing this innovative framework, a new set of incentives can be established, making truth more profitable than fiction, at scale. The barriers that have traditionally separated engineers and scientists will no longer obstruct the curation of information essential to the insurance industry for crafting effective and socially impactful insurance products. This platform operates under a set of rules that apply equitably to all participants, eradicating corruption and unnecessary friction. Crucially, it provides the insurance industry with a reliable baseline of data to train AI models accurately, ensuring they operate in the right place, at the right time, and at the right price.

Visionary Leaders

The Ingenesist Project seeks sponsors to expedite the development of the “Innovation Bank.” Additionally, directorships and governance positions are available for visionary leaders in the insurance and engineering fields who recognize the potential of this groundbreaking initiative.

Artificial Intelligence (AI) is frequently mentioned for its capacity to blur the lines between facts and fiction. Numerous articles envision a future in which AI bots construct believable scenarios without relying on direct observation. Many instances illustrate the potential pitfalls of this. So, if AI can excel at finding the best incorrect answer, why can’t it excel at finding the best correct answer?

In this early stage of widespread AI and machine learning adoption, many proponents acknowledge the necessity of human involvement in the learning process. This raises the age-old question: “Who can we trust?” This is especially pertinent when the incentive is to replace humans with machines. The enduring challenge (and opportunity) is to avoid wholesale human replacement and instead focus on enhancing human abilities with the aid of new technology.

Economics is fundamentally driven by incentives.

The Ingenesist Project’s Innovation Bank provides an ideal environment for AI and machine learning to prioritize facts over fiction. Through a strategic blend of game theory, blockchain technology, and AI, The Innovation Bank introduces an alternative set of incentives that guide participant actions. The Innovation Bank serves as a self-regulating truth engine, safeguarding society against malicious actors attempting to disseminate unfounded or fraudulent claims.

A Multi-Agent Algorithmic Game:

In essence, The Innovation Bank operates as a game in which participants make claims about the state of the world, which must then be validated by other participants. Each participant is rewarded with an electronic token for creating an immutable node on a network graph. As the network expands, the graph accumulates increasingly valuable business intelligence. Accessing this intelligence requires the expenditure of tokens, potentially purchased by institutional users from a third-party clearinghouse. This system eliminates incentives for cheating.

Natural Language Processing (NLP):

AI-powered NLP algorithms can scrutinize the language used in node creation, detecting patterns, inconsistencies, or suspicious elements. NLP models understand context and semantics, enabling them to identify potential fraud or falsehoods. NLP also assists in verifying claims by cross-referencing them with external sources (validating the validator).

Data Analysis and Pattern Recognition:

AI can process and analyze vast amounts of blockchain data to uncover patterns and anomalies. By comparing multiple claims and validations, AI can identify discrepancies or abnormal behavior indicative of fraud. These capabilities help distinguish genuine claims from fraudulent ones, with no incentive for dishonesty.

Image and Video Analysis:

In cases involving visual evidence, AI employs computer vision techniques to analyze images or videos for authenticity. AI assesses image metadata, detects alterations, and evaluates facial expressions and body language to spot potential manipulation or fraud. Here, the condition arises where crafting a believable falsehood becomes more expensive than simply presenting facts.

Network Analysis:

AI examines the connections between nodes in the blockchain network, identifying suspicious networks or clusters that suggest collusion or fraud. This analysis sheds light on the credibility and trustworthiness of suspect nodes.

Continuous Learning and Adaptability:

AI systems continuously learn from new data, adapting algorithms to evolving fraudulent tactics. Machine learning enhances accuracy in distinguishing truth from fraud, even as the system encounters new forms of deception.

Risk Scoring and Fraud Detection:

AI assigns risk scores to nodes based on factors like proximity to other nodes, validation history, and information consistency. Predictive models identify high-risk nodes or validations, alerting the system to isolate these sources.

Conclusion:

A new economic framework can be seamlessly integrated into existing business methods, creating a condition where falsification is costlier than authenticity. This sharpens the blurry line between fact and fiction. Under this condition, AI can play a vital role in discerning fact from fiction by tracking the creation, circulation, and adoption of digital receipts. AI’s analytical prowess, pattern recognition, and continuous learning ensure the system remains robust at isolating fraudulent activities. The combination of blockchain technology and AI-driven analysis forms a potent framework for curating truthful information and upholding system integrity.

Artificial Intelligence is widely cited for the potential to spoof facts with fiction. Countless articles predict a world where AI bots craft statistical plausibility in the absence of direct observation. Countless examples demonstrate how this can go terribly wrong. So, If AI can be used to find the best wrong answer, why can’t it be used to find the best right answer?

At this early stage of widespread adoption of artificial intelligence and machine learning (AI/ML), many proponents have conceded that human involvement in the learning protocol will be necessary. This leads to the age old problem of: “who do you trust?” – especially where the incentive is to replace humans with machines. The age-old challenge (and opportunity) will be to resist the wholesale replacement of humans and focus on creating a higher order where humans ability is amplifies with the assistance of new technology.

Economics is the Science of Incentives

The Innovation Bank creates an environment ideally suited for AI/ML to anchor facts over fiction. Using a strategic combination of game theory, blockchain, and AI, The Innovation Bank introduces an alternate set of incentives under which participants will operate. The Innovation Bank forms a self-regulating truth engine that can safeguard the health and welfare of society against malicious actors actively trying to pass off unfounded or fraudulent claims.

Multi-Agent Algorithmic Game

Briefly described, the Innovation Bank is a game where players make claims about the state of the world. These claims must then be validated by another player. Each player is then rewarded an electronic token for producing an immutable node on a network graph. As the network grows, its graph stores increasingly valuable business intelligence. In order to access this business intelligence, one must expend tokens. Institutional users would likely need to purchase tokens from a 3rd party clearinghouse listing from those who may seek to liquidate their tokens, thereby giving them a market value based on supply and demand. There is no incentive to cheat.

Natural Language Processing (NLP):

AI-powered NLP algorithms can analyze the language used in the formation of nodes, looking for patterns, inconsistencies, or suspicious elements. By understanding the context and semantic meaning of the text, NLP models can identify potential instances of fraud or falsehoods. NLP can also assist in verifying claims by cross-referencing them with external sources of information (validating the validator).

Data Analysis and Pattern Recognition:

AI can process and analyze large volumes of data within the blockchain to identify patterns and anomalies. By comparing multiple claims and validations, AI algorithms can detect and isolate discrepancies or abnormal behavior that may indicate fraudulent activities. These analytical capabilities help in distinguishing genuine claims from fraudulent ones. Again, there is no incentive to cheat.

Image and Video Analysis:

In scenarios where claims involve visual evidence, AI can employ computer vision techniques to analyze images or videos and determine their authenticity. AI algorithms can assess image metadata, detect alterations, or analyze facial expressions and body language to identify and isolate potential manipulations or fraudulent content. An essential condition is reached where forming a viable falsehood is more expensive than simply providing fact.

Network Analysis:

AI can examine the relationships and connections between nodes in the blockchain network. By analyzing the patterns of validations and associations, AI algorithms can identify suspicious networks or clusters that might indicate collusion or fraudulent behavior. This network analysis provides valuable insights into the credibility and trustworthiness of suspect nodes.

Continuous Learning and Adaptability:

AI systems can continuously learn from new data and adapt their algorithms to evolving fraudulent techniques. By leveraging machine learning, AI models improve over time, becoming more accurate in distinguishing between truth and fraud. As the system encounters new types of fraud, AI can detect emerging patterns and update the validation mechanisms accordingly.

Risk Scoring and Fraud Detection:

AI can assign risk scores to specific nodes based on various factors, such as proximate to other nodes, validation history, and the consistency of information. By utilizing predictive models, AI can identify high-risk nodes or validations, alerting the system to isolate that particular source node.

Conclusion:

A new economic game can be easily inserted to existing business methods to create the essential condition where falsification is more expensive than authenticity. Under this condition, AI can become very useful in isolating fact over fiction by simply tracking the creation, circulation, and uptake of digital receipts. AI’s analytical capabilities, pattern recognition, and continuous learning ensure that the system remains robust and effective in isolating fraudulent activities. The combination of blockchain technology and AI-driven analysis forms a powerful framework for curating truthful information and maintaining the integrity of the system.

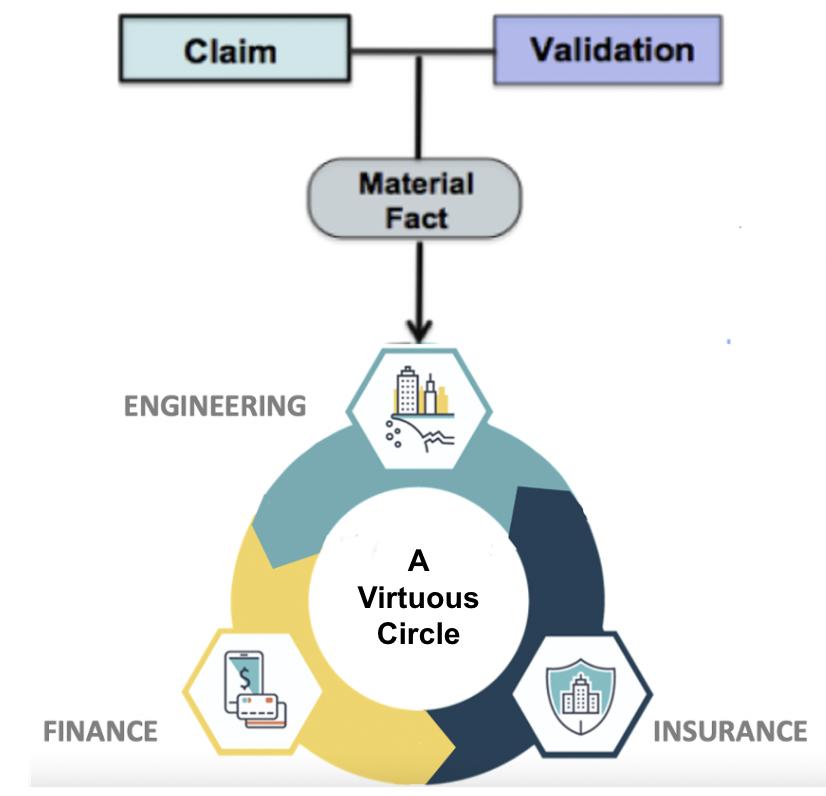

In the realm of economic development, the interplay between banking, insurance, and engineering forms a virtuous circle that drives modern civilization forward. However, the crucial role played by engineers, scientists, and technicians in this cycle is often overlooked in economic discourse. Their primary responsibility is to produce material facts, which involves identifying risk exposure, calculating the probability of risks materializing, and assessing the consequences of failures. When these components are harmoniously integrated, finance, insurance, and engineering can collectively support the sustainable and peaceful habitation of our world.

The Virtuous Circle of Economic Sustainability

The Importance of Material Facts:

Material facts are integral to decision-making processes. They are facts whose suppression could reasonably lead to different decisions. However, in our increasingly polarized society, the dissemination of disinformation poses a significant threat to the integrity of material facts. Counteracting this challenge becomes even more complex considering that technology facilitates the creation and widespread distribution of misinformation at an unprecedented scale. Meanwhile, securing material facts requires adherence to a specific sequence, a standard of proof, and an immutable record. This presents a simple problem in need of a solution.

The Role of AI in Securing Material Facts:

Enter the Innovation Bank—an initiative that leverages AI to curate and integrate validated material facts across diverse physical conditions, preempting the risk of disinformation. By acting as a formidable gatekeeper, this powerful system establishes a filter through which disinformation must pass to attain credibility. The value of such a “disinformation filter” transcends individual projects and encompasses the entire economy. Building this AI-driven solution is not only feasible but also imperative.

Join the Movement:

To learn more about the projects spearheaded by The Innovation Bank and contribute to this transformative endeavor, reach out to The Ingenesist Project. Together, we can construct a robust foundation that promotes economic stability, fosters material facts, and guards against the perils of disinformation.

In the ever-evolving landscape of technology, artificial intelligence (AI) plays a crucial role in enhancing the effectiveness and efficiency of various systems. The Value GameTM, powered by The Innovation Bank™, is no exception. By incorporating AI algorithms and machine learning capabilities, these groundbreaking platforms from The Ingenesist Project can further revolutionize the way we establish trust, verify claims, and combat fraud in real life systems that sustain civilization.

Patterns of Fact

AI can be employed in multiple stages of The Value Game to strengthen its integrity. Firstly, AI algorithms can assist in the initial claim recording process by automatically cross-referencing the information provided with existing databases, verifying its accuracy and authenticity. This reduces the burden on human validators and enhances the speed and accuracy of claim validation. Furthermore, AI can analyze patterns and detect any inconsistencies or red flags in claims, providing an additional layer of security and fraud detection.

Patterns of Fraud

As The Value Game accumulates a vast amount of data on claims and validations, AI algorithms can continuously analyze this information to identify trends and anomalies. By learning from past instances, AI can identify potential fraudulent behavior, detect patterns of collusion, and even predict future attempts at deceit. This proactive approach allows the system to stay one step ahead of attackers, making it increasingly challenging for them to exploit the platform.

Network of Trust

Moreover, AI can contribute to the ongoing curation of claims and validations. By analyzing the data collected, AI algorithms can identify correlations between different claims, validators, and professions. This analysis helps build a comprehensive network of trust, providing participants with a broader context and enabling them to make more informed decisions when validating claims. AI-powered insights can guide participants in identifying outliers and potential risks, fostering a more secure and reliable environment.

Transaction of Records

Additionally, AI algorithms can assist in assessing the reputation and credibility of participants within The Value Game. By analyzing historical data and interactions, AI can assign reputation scores to individuals based on their track record of accurate validations or fraudulent claims. These reputation scores can serve as an additional factor in evaluating the credibility of a claim or a validator, further strengthening the overall trustworthiness of the system.

Things that get better with age

With the integration of AI, The Value Game becomes a dynamic and self-improving ecosystem. As more data is collected and analyzed, AI algorithms continuously refine their models, improving the accuracy of fraud detection and claim validation. This iterative process enhances the system’s resilience and adaptability, enabling it to keep up with emerging tactics employed by attackers.

Adapting diverse datasets

The incorporation of AI into The Value Game also extends its applicability beyond traditional fields and professions. While initially focused on STEM professionals, the AI-powered platform can expand to cover a broader range of domains. By training the AI models on diverse datasets from various fields, the system can adapt to accommodate claims and validations across different industries, thus maximizing its impact and relevance.

A sophisticated and resilient platform

In conclusion, by harnessing the power of AI, The Value Game evolves into a sophisticated and resilient platform that effectively combats fraud and deception in real life systems. AI algorithms contribute to the initial claim validation, continuous curation, fraud detection, and reputation assessment, enhancing the overall trustworthiness and reliability of the system. With AI as its ally, The Value Game becomes a powerful tool that empowers individuals, safeguards authenticity, and enables trust to flourish in an increasingly interconnected world.

An engineer’s role is to mitigate risks in complex systems. Activities like flying through the sky, transplanting organs, and fiddling with energy are very risky indeed. The primary output of an engineer is the removal of these risks. It’s a straightforward concept: Engineers remove risk from complex systems.

A firefighter is worth a million dollars per hour safeguarding life and property – when there is a fire. The value of the firefighter is easily measured by severity of the fire. A fire protection engineer can design thousands of buildings that will never burn. Unfortunately, in the absence of a fire, there is no way to measure the true economic value of the engineer?

Reflecting on the complex global challenges that civilization faces: Are we fighting fires or solving fires?

Unless we accurately assess the economic value of engineers and incorporate it into our monetary system, it will always be more profitable to allow the world to burn.

Engineers remove risk from complex systems – this idea is easy to understand and the solution is actually quite simple – we have the technology and analysis tools to accomplish this with relative ease.

Please lend your support to The Ingenesist Project by contacting us directly for full specifications of this project, or by pitching in with the PayPal link above. If we don’t fix it, who will?

The process is so simple, it defies the imagination.

Countless words have been written about the nature of money and its role in society. Ultimately, money serves as a representation of human productivity, as people work and produce goods and services in exchange for it. The creation of money is based on the things we produce, allowing us to measure its value.

Banks address the time gap between production and payment by creating an asset called “future productivity.” This asset enables them to generate money before the actual goods or services are produced. It takes the form of debt.

However, innovation also represents future productivity, as it brings forth useful things that have not yet been created. In fact, approximately 80% of economic growth can be attributed to technological advancements. So, why can’t engineers adopt a similar approach to banks and measure money into existence? This would serve as a means of bridging the time gap and funding the substantial amount of innovation necessary to sustain our world.

Although it may seem like a straightforward idea, it is challenging to comprehend. The issue lies not in a broken world but in a broken monetary system. The solution lies in fixing this system.

To address these challenges and promote innovative solutions, please lend your support to The Ingenesist Project. We literally make money.

A bank will not lend money to a project unless it is insured. An insurance company will not insure a project unless it is well engineered. Engineering cannot be well done without a bank to cover soft costs. Together, this forms the virtuous circle of modern civilization.

While the banking and insurance piece seems straight forward, very few economic journals discuss the role of engineers, scientists, and technicians in this manner. Their role is to produce material fact:

1. Identify the risk exposure,

2. calculate the probability that risk will manifest,

3. review and assess consequences in the event that the peril does manifest.

Done correctly, finance, insurance, and engineering can sustain the indefinite peaceful habitation of the world.

The War on Facts:

If any of these three pieces are missing, distorted, or corrupted, the economics collapses, projects fails, and things blow up.

A material fact is a fact, the suppression of which would reasonably result in a different decision.

Wikipedia

As we increasingly endure a polarized society where disinformation is spread with precisely the intention of distorting material facts, nothing could be more important than a means for securing material facts. This is a simple idea.

There is the further disadvantage that technology itself vastly favors the cheap creation and distribution of misinformation – at scale – while securing material facts must be committed in a certain sequence, standard of proof, and immutable record. This is a simple problem to solve.

The Innovation Bank curates and integrates validated material fact across a range of physical conditions prior to the peril of disinformation occurring. Such a powerful gauntlet may provide a sieve through which disinformation must survive in order to establish credibility. The value of such a “disinformation filter” amounts to the value of our economy at large. This is simple. This is serious. This is something that we can build today.

Please contact and contribute to The Ingenesist Project for more information about The Innovation Bank projects.

The Innovation Bank is a novel method of business related to the integration and capitalization of knowledge assets. The Innovation Bank is an application of game theory, actuarial math and a simple native “proof-of-stake” blockchain. The system aims to unify the global engineering and scientific disciplines by incentivizing individual practitioners to form knowledge asset networks among each other by producing claims and validations related to physical, measurable, and observable facts. Each claim and associated validation forms a node in a network for which each participant is awarded a cryptographic token memorializing earned stake (equity) in the system. A secure, validated, and decentralized knowledge repository and access management system is secured by a simple native blockchain. Revenue is generated through the liquidation of earned tokens on an external market to third parties seeking access to network metadata for business intelligence. The intrinsic value of the network grows as the number of participants increases. As participation increases, the quantity and quality of the transaction records also increases. Third-party buyers may include banks, insurance companies, and private enterprise.

In the United States, the term “Engineer” is regulated by licensure boards, which means it refers to a person who is registered and licensed to practice engineering in the country. However, for everyone else, there is no clear definition.

The elusive nature of the term “Engineer” raises questions. Does it refer to someone licensed to practice in a specific jurisdiction? Or is it someone who has completed four or five years of university education? Does it encompass those who operate complex machinery like locomotives, sound boards, or building systems?

Considering that the engineering profession is responsible for nearly 80% of economic growth, it becomes crucial to establish a precise, measurable, and actionable definition. Without a rigorous definition, it is difficult to effectively manage the profession. These gaps in definition are significant oversights.

Given the lack of a suitable synonym for “Engineer,” we introduced the term “Ingenesist” with the following explanation:

The Latin word for engineer is “Ingeniator,” which is derived from two other Latin words: “ingenaire” (to conceive or derive) and “ingenium” (cleverness). The suffix “-ist” implies someone or something characterized by a specified quality. Combining these elements, an Ingenesist can simply be defined as a “creator of useful things.”

This straightforward definition is superior in describing the essence of engineering and its problem-solving nature. It can be put into action from an economic, political, or legal perspective, as there are rigorous definitions for what is considered useful and what is not. Importantly, this definition does not contradict existing conventions or institutions. It includes licensed and unlicensed professionals, as well as those from international backgrounds or those who rely on intuition rather than formal education in understanding the laws of nature. The term “Ingenesist” encompasses artists, craftsmen, technologists, and more.

Most importantly, the concept of an Ingenesist is inclusive rather than exclusive. It is accessible to anyone who chooses to be productive in a useful manner. Differentiating between what is useful and what is not comes naturally when using the term Ingenesist. It acknowledges the innate creative nature of our species.